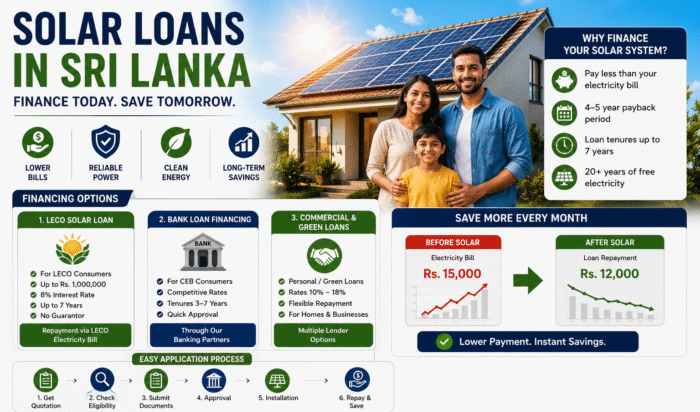

Solar Loans in Sri Lanka: Interest Rates, Eligibility & Best Financing Options

The upfront cost of a solar system is the single biggest barrier stopping Sri Lankan households and businesses from making the switch. Yet in many cases, the monthly loan repayment for a solar installation works out to less than the electricity bill it replaces — meaning you can go solar with no net increase in monthly outgoings, and own a valuable asset at the end of the loan term.

This guide covers everything you need to know about solar loans in Sri Lanka: the schemes available, interest rates, eligibility requirements, and how to choose the financing option that makes the most sense for your situation.

Why Solar Financing Makes Financial Sense in Sri Lanka

Going solar is one of the few investments where the asset you purchase actively pays for itself. A correctly sized solar system reduces or eliminates your electricity bill from the moment it is commissioned. If your monthly loan repayment is Rs. 12,000 and your previous electricity bill was Rs. 15,000, you are immediately cash-flow positive — paying less each month than before, while building ownership of a system that will generate free electricity long after the loan is repaid.

The average payback period for a solar installation in Sri Lanka is 4–5 years. Bank loan tenures for solar financing commonly run 5–7 years. This means that by the time your loan is paid off, you are already approaching the point where the system has recovered its full cost — and the remaining 15–20 years of panel life deliver electricity at zero fuel cost.

Explore the full range of solar financing options available through St. Anthony’s Solar to understand which scheme fits your profile best.

Solar Loan Schemes Currently Available in Sri Lanka

1. LECO Solar Loan Scheme (Sooryabala Sangramaya)

The Lanka Electricity Company Limited (LECO) has introduced a dedicated solar loan scheme for eligible consumers under the government’s Sooryabala Sangramaya (Battle for Solar Energy) initiative — a programme designed to install micro solar units in one million homes across Sri Lanka and contribute significantly to the national grid through renewable energy.

Key loan details:

- Available to LECO domestic consumers only (CEB consumers are not eligible under this specific scheme)

- Eligibility: consumers whose average monthly electricity bill exceeds Rs. 3,000, or is expected to exceed that threshold

- Maximum loan amount: Rs. 1,000,000 (1 million)

- Interest rate: 8% per annum

- Repayment period: 7 years, collected through the monthly LECO electricity bill

- No guarantors required

Loan disbursement conditions:

- For loan amounts below Rs. 500,000: 90% is covered by the loan; the customer pays the remaining 10%

- For loan amounts below Rs. 1,000,000: 75% is covered by the loan; the customer pays 25%

- For the maximum loan amount of Rs. 1,000,000: the customer must contribute more than 25%, with the remainder covered by the loan

This scheme is available for a limited period and funds are allocated to the first 2,000 qualifying customers. If you are a LECO consumer considering solar, this is one of the most accessible and low-cost financing routes currently available.

Additional benefit under the programme: Any surplus electricity generated within the first 7 years is purchased at Rs. 22.00 per unit, and after the 7th year at Rs. 15.50 per unit — providing an income stream on top of bill elimination.

2. Bank Loan Financing Through St. Anthony’s Solar’s Banking Partners

For CEB consumers and those who do not qualify for the LECO scheme, bank-facilitated solar loans offer an accessible alternative. St. Anthony’s Solar works with established local banking partners to help customers access solar financing with competitive terms.

These loans are processed through the company’s network of bank partners, and the team assists customers through the application and approval process. Interest rates, loan tenures, and repayment structures vary by bank and customer profile — speaking directly with the team at St. Anthony’s Solar is the most efficient way to identify which bank partner and loan product suits your situation.

3. Commercial Bank & Development Finance Loans

Beyond scheme-specific financing, several Sri Lankan commercial banks and development finance institutions offer personal loans, green loans, or housing-linked loans that can be directed toward solar installations. These typically carry interest rates ranging from 10% to 18% depending on the institution, loan type, and customer credit profile.

The advantage of going through a reputable solar installer like St. Anthony’s Solar is that they can guide you to the most suitable lender and help you prepare the documentation needed for a swift approval.

How to Apply for a Solar Loan in Sri Lanka: Step-by-Step

Step 1 — Get a system quotation first. Before approaching a bank or loan scheme, you need to know how much your solar installation will cost. Request a free site assessment and quote from a registered solar installer. This document is required by lenders to process your application.

Step 2 — Identify the right loan scheme. Determine whether you are a LECO or CEB consumer — this immediately narrows your options. LECO consumers should explore the Sooryabala Sangramaya scheme first given its favourable 8% interest rate and no-guarantor requirement. CEB consumers should explore bank partner financing.

Step 3 — Check your eligibility. For the LECO scheme, confirm your average monthly bill exceeds Rs. 3,000. For bank loans, gather your income documentation, utility bills, and any property ownership documents that may be required.

Step 4 — Prepare your documents. Typically required documents include your national identity card, recent electricity bills (last 3–6 months), proof of income or employment, the solar installation quotation, and in some cases a property deed or rental agreement.

Step 5 — Submit the application. For the LECO scheme, download the official Sooryabala Sangramaya application form (available through St. Anthony’s Solar’s financing page) and submit it with the required documents. For bank financing, your installer’s team will guide you through the relevant bank’s process.

Step 6 — Await approval and valuation. The bank or scheme administrator reviews your application. For LECO loans, the process is relatively streamlined given the fixed scheme structure. Bank loans may involve additional credit checks.

Step 7 — Loan disbursement and installation. Once approved, funds are typically disbursed directly to the solar installer. Installation is then scheduled and completed, usually within a few days for residential systems.

Step 8 — Begin repayments and track savings. Repayments begin the following month. Compare your new monthly outgoing (loan repayment) against your previous electricity bill — in most cases, the net difference is immediately favourable or neutral, and improves further as electricity tariffs rise.

How to Choose the Best Solar Financing Option: A Practical Guide

Not all solar loans are equal, and choosing the wrong one can reduce the financial benefit of going solar. Here is how to evaluate your options:

Compare the effective cost of borrowing. An 8% interest rate over 7 years is significantly more affordable than a 16% personal loan over 3 years, even if the monthly repayments look similar on the surface. Always calculate the total amount repaid over the loan life, not just the monthly instalment.

Match the loan tenure to the payback period. Ideally, your loan should not outlast the point at which your solar system has paid for itself. A 5–7 year loan on a system with a 4–5 year payback is optimal — you reach payback before or around the time the loan ends.

Consider whether your monthly repayment is less than your current bill. If the monthly loan repayment exceeds your current electricity bill significantly, reconsider the system size or loan structure. The goal is for the repayment to be comfortably covered by your bill savings.

Check for early repayment terms. Some loans allow early settlement without penalty. If you receive a lump sum or windfall during the loan period, early repayment can reduce total interest paid considerably.

Use a trusted installer as your financing partner. Banks and scheme administrators are more likely to approve applications supported by reputable, registered solar companies. St. Anthony’s Solar’s established relationships with local banking partners streamline the approval process and help ensure you are matched with the most suitable financing product for your needs. Get in touch with the team to begin the process.

Frequently Asked Questions: Solar Loans in Sri Lanka

Who is eligible for the LECO solar loan scheme? Only LECO domestic consumers are eligible. Your average monthly electricity bill must exceed Rs. 3,000, or be expected to do so. CEB consumers are not eligible for this specific scheme and should explore bank financing alternatives.

What is the interest rate on solar loans in Sri Lanka? The LECO Sooryabala Sangramaya scheme offers 8% per annum — one of the lowest rates available for solar financing in Sri Lanka. Bank loans vary between approximately 10% and 18% depending on the institution and loan type.

Do I need a guarantor for a solar loan? Under the LECO scheme, no guarantor is required. For bank loans, requirements depend on the specific lender and your credit profile — some products require a guarantor, others do not.

How long is the repayment period? The LECO scheme runs for 7 years, with repayments collected through your monthly LECO electricity bill. Bank loan tenures typically range from 3 to 7 years.

Can I get a solar loan if I am self-employed? Yes, though the documentation requirements may differ from salaried employees. Bank lenders typically require income statements, tax returns, or business financial records. Working through an installer with established banking relationships helps navigate this process more smoothly.

Is there a maximum loan amount for solar financing? Under the LECO scheme, the maximum is Rs. 1,000,000. Under bank financing, the amount depends on your income, creditworthiness, and the lender’s policies — in practice, most residential solar systems fall comfortably within standard personal or green loan limits.

What happens if I sell my property during the loan period? This depends on the loan structure. For LECO loans repaid via the electricity bill, the obligation is tied to the LECO account rather than the property. For bank loans, the solar asset and the loan remain with the borrower unless otherwise agreed. Discuss this scenario with your lender before signing.

Can a business take a solar loan in Sri Lanka? Yes. Commercial and industrial solar financing is available through banking institutions, often under green lending or SME loan frameworks. Terms differ from residential financing — a solar installer experienced in commercial projects can advise on the most suitable approach.

What documents are needed to apply? Typically: national identity card, last 3–6 months of electricity bills, proof of income, a formal quotation from the solar installer, and in some cases a property deed or rental agreement. The exact list depends on the lender.

How quickly can a solar loan be approved? The LECO scheme has a structured process with defined timelines. Bank loans typically take 1–3 weeks from complete application submission to approval. Working with an experienced installer who has established bank relationships can significantly speed up this timeline.

Most Searched Topics: Solar Loans in Sri Lanka

Solar loan interest rate Sri Lanka 2025: The lowest currently available rate through a government-backed scheme is 8% per annum under the LECO Sooryabala Sangramaya programme. Commercial bank loans for solar typically range from 10–18% depending on the product and borrower profile.

Can I get a solar loan without a guarantor Sri Lanka: Yes — the LECO scheme specifically requires no guarantor. Some bank products also offer guarantor-free options for qualified borrowers.

Best bank for solar loan Sri Lanka: The best option depends on whether you are a LECO or CEB consumer, your income profile, and the loan amount needed. St. Anthony’s Solar works with multiple local banking partners and can help identify the most suitable lender for your situation.

Solar loan repayment through electricity bill Sri Lanka: Under the LECO Sooryabala Sangramaya scheme, monthly repayments are collected directly through your LECO electricity bill over 7 years — simplifying the repayment process with no separate bank standing order needed.

Sooryabala Sangramaya eligibility and how to apply: The scheme is open to LECO domestic consumers with monthly bills above Rs. 3,000. Application forms are available through registered solar installers like St. Anthony’s Solar. Only the first 2,000 qualifying customers receive funding under this limited-period programme.

Solar financing for businesses Sri Lanka: Commercial solar financing is available through green lending and SME loan programmes at several Sri Lankan banks. System sizes for commercial applications typically start at 15–20 kW and scale up significantly for industrial consumers.

Conclusion

The most common reason people delay going solar is the perceived barrier of upfront cost. But with solar loans in Sri Lanka now available through government-backed schemes and banking partners — many with interest rates as low as 8% and no guarantor requirement — that barrier is lower than most people realise.

When the monthly loan repayment is less than the electricity bill it replaces, solar financing does not cost you money. It restructures your energy expenditure into an asset-building investment, with free electricity at the end of the loan term and for decades beyond.St. Anthony’s Solar helps customers navigate the full financing process — from identifying the right loan scheme and preparing documentation, to installation and ongoing support. If you are ready to explore your options, speak with the St. Anthony’s Solar team today for a free consultation and tailored financing guidance.